We will develop models for all Exchanges (NSE, NASDAQ etc), all Instruments (Equity, Forex, Commodity, and Derivatives etc), all Time Frames (Intraday, Week, Short Term, Long Term etc) and for all Market Participants (Arbitragers, Hedgers, Speculators etc) and also for all Market Types (Bullish, Bearish and Sideways)

Market Making

Exchange Arbitrages

Arbitrages

Statistical Arbitrage

High Frequency Trading models

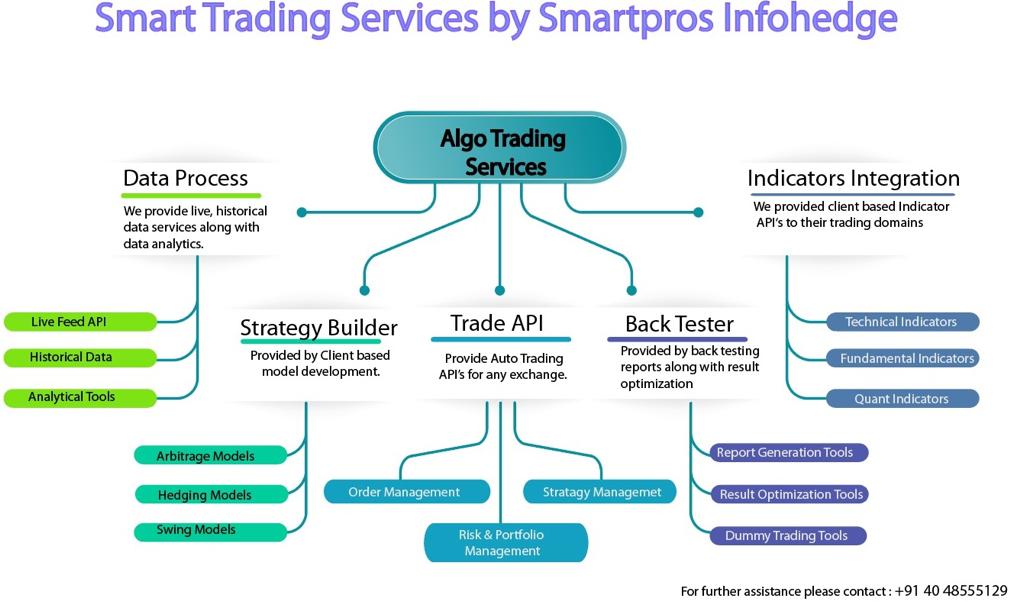

Strategy Building

Greeks Dynamic Hedging

Portfolio Management

Risk Management

Hypothesis (Know about Market Insight)

Modeling (Input Analysis parameters )

Model validation( Back Test and Modifications)

Analysis & Strategy Building

Entry (Bid-Ask Spread, Leg Sequence, Liquidity etc)

Trade Management (Risk Parameters, Latest Market Info etc)

Exit (Profit or Stop)

Clean data

Align time stamps

Read Gigabytes of data

Extract relevant information

Handle missing data

Incorporate events, news and announcements

Code up the quant. Strategy

Code up the simulation

Wait a very long time for the simulation to complete

Recalibrate parameters and simulate again

Wait a very long time for the simulation to complete

Recalibrate parameters and simulate again

Wait a very long time for the simulation to complete

Back testing simulates a strategy (model) using historical or fake (controlled) data.

It gives an idea of how a strategy would work in the past.

It gives an objective way to measure strategy performance.

It generates data and statistics that allow further analysis, investigation and refinement.

It helps choose take-profit and stop loss.

Profit Loss

Mean, stdev, corr

Sharpe ratio

Confidence intervals

Max drawdown

Breakeven ratio

Biggest winner/loser

Breakeven bid/ask

Slippage

Allow easy strategy programming

Allow plug-and-play multiple strategies

Simulate using historical data

Simulate using fake, artificial data

Allow controlled experiments

Generate standard and user customized statistics

Have information other than prices

Auto calibration

Sensitivity analysis

Quick

Back testing generates a large amount of statistics and data for model analysis.

We may improve the model by

Regress the winning/losing trades with factors

Identify, delete/add (in)significant factors

Check serial correlation among returns

Check model correlations

The list goes on and on……

© 2019 SmartPro Infohedge All rights Reserved.